Introduction

Starting your investment journey can feel intimidating. You might wonder when to buy, how much to invest, and whether you’re getting in at the right time. These questions often cause fear and hesitation. That’s where dollar cost averaging comes in. It offers a solution that’s especially helpful for new investors. This strategy helps reduce risk, eliminates the pressure of timing the market, and builds consistency. In this guide, we’ll explain what dollar cost averaging is for beginners, why it works, and how to use dollar cost averaging for long-term investing. Whether you’re investing in stocks, ETFs, or crypto, this approach can help make your journey smoother and more successful.

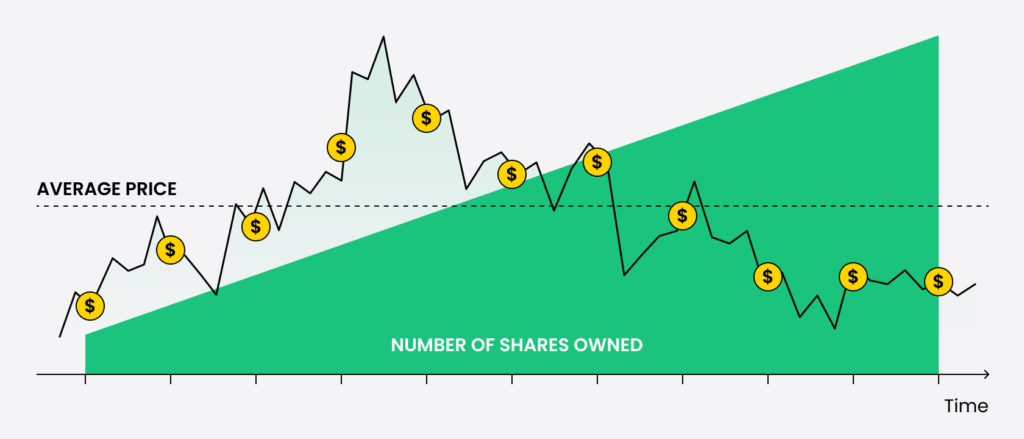

What Is Dollar Cost Averaging?

Dollar cost averaging (DCA) is an investing technique where you invest a fixed amount of money into an asset on a regular schedule—regardless of its price. The idea is simple: instead of trying to guess when prices will go up or down, you make consistent investments over time. That means sometimes you’ll buy more when prices are low and less when prices are high. Eventually, this can lower your average cost per share.

Let’s say you want to invest $1,200 in an ETF. You could either invest the full amount today or break it up into $100 every month for 12 months. By doing the latter, you avoid the risk of putting all your money into the market at a bad time. Over time, the highs and lows balance out, giving you a smoother average entry point.

Dollar cost averaging doesn’t guarantee profits, but it does help reduce the impact of volatility. It also promotes long-term thinking, which is key for any successful investor. More importantly, it removes emotions from your decision-making—one of the most common pitfalls in investing.

Why Dollar Cost Averaging Matters for Beginners

When you’re new to investing, the stock or crypto markets can look intimidating. Markets go up and down every day. Prices are unpredictable. News headlines stir emotions. It’s tempting to wait for “the perfect time” to enter the market. But the truth is, no one can time the market consistently. Not even professionals.

That’s what makes dollar cost averaging so powerful. It removes the need to predict. Instead, it turns investing into a habit. You’re not reacting to headlines or market swings. You’re simply following a plan.

This strategy is especially important for beginners because it:

- Reduces the risk of investing a lump sum right before a downturn

- Helps you avoid emotional buying and selling

- Encourages regular saving and consistent contributions

- Builds long-term investing habits

- Makes market volatility work in your favor over time

By using dollar cost averaging, you focus less on market timing and more on building a portfolio that grows steadily over the years. That mindset shift is what separates successful investors from everyone else.

How Dollar Cost Averaging Works in Practice

Now that you understand the concept, let’s see how it works in real life. Here’s an example:

Suppose you decide to invest $200 into Bitcoin every month. In January, Bitcoin is $40,000, so you buy 0.005 BTC, In February, it drops to $35,000, so you get about 0.0057 BTC. In March, it rises to $45,000, and you get 0.0044 BTC. Over time, you accumulate more BTC when the price is low and less when the price is high. Your average cost smooths out, and you reduce the impact of price swings.

This method also works with stocks, mutual funds, ETFs, or any asset that allows fractional purchases. You don’t need to worry about minimum share prices. Most brokerages now allow you to buy partial shares, so even small amounts are enough to get started.

Steps to Start Using Dollar Cost Averaging Today

Starting your DCA strategy is easy, even if you’ve never invested before. Just follow these steps:

1. Set Your Budget

Start by figuring out how much you can invest consistently. It could be $25 per week, $100 per month, or even $10 per day. The specific amount doesn’t matter as much as your ability to stick to it. Choose a number that won’t stretch your finances. It’s better to start small and build the habit than overcommit and stop halfway.

2. Pick a Schedule

Decide how often you want to invest. Most beginners prefer monthly or biweekly investments since it aligns with paydays. Others prefer weekly contributions for more frequent exposure. There’s no wrong choice here—what matters is that you pick a schedule you can stick with for months or years.

3. Choose What to Invest In

Now it’s time to decide where your money will go. For beginners, index funds and ETFs are often the best choices. They offer instant diversification, low fees, and steady growth. However, DCA also works with individual stocks, cryptocurrencies, or even commodities. Just make sure the asset matches your risk tolerance and long-term goals.

Some common beginner-friendly options include:

- S&P 500 index funds (like VOO or SPY)

- Total market ETFs (like VTI)

- Bitcoin or Ethereum for crypto exposure

- Dividend-paying stocks for income

- Target-date funds for long-term growth

4. Automate the Process

Automation is the secret weapon of dollar cost averaging. Most brokerage platforms allow you to set recurring transfers. You can schedule automatic investments into your chosen asset every week or month. This helps remove the temptation to time the market or skip a month.

Once it’s automated, investing becomes something that happens in the background—just like paying your bills. You’ll barely notice the money leaving your account, but your portfolio will grow over time.

5. Stay Consistent and Ignore the Noise

Markets will rise. Markets will fall. Prices will soar. Prices will crash. Through it all, your job is to stay the course. Dollar cost averaging only works if you keep going—especially during the dips. Many investors panic and stop investing when the market drops. But that’s often the best time to buy.

The key is discipline. Trust the process. Stick to your plan. The longer you invest consistently, the more likely you are to benefit from long-term growth.

Benefits of Dollar Cost Averaging Over Lump Sum Investing

You might wonder: why not just invest everything at once? Isn’t that faster? The answer depends.

Historically, lump sum investing has slightly outperformed DCA over long periods—if the market is rising. However, not everyone has a large lump sum to invest. More importantly, lump sum investing carries more short-term risk. If you invest $10,000 right before a market crash, you could lose a significant chunk quickly.

That’s why many beginners prefer DCA. It reduces short-term risk, builds confidence, and encourages long-term thinking. It’s also perfect for people who invest from their salary each month, which is the case for most workers.

Here’s a quick comparison:

| Feature | Dollar Cost Averaging | Lump Sum Investing |

|---|---|---|

| Emotional control | High | Low |

| Risk of bad timing | Lower | Higher |

| Long-term returns | Slightly lower | Potentially higher |

| Best for | Beginners, cautious | Confident, experienced |

Who Should Use Dollar Cost Averaging?

Dollar cost averaging isn’t just for beginners—it’s useful for anyone who wants a low-stress approach to investing. It works especially well for:

- New investors building their first portfolio

- Employees investing a portion of each paycheck

- Anyone nervous about market volatility

- People without a large lump sum to invest

- Long-term investors focused on growth over decades

If you fit any of those categories, dollar cost averaging might be the right strategy for you.

Mistakes to Avoid When Using Dollar Cost Averaging

Although DCA is simple, beginners can still make mistakes. Be sure to avoid the following:

- Stopping during a downturn: Market dips are normal. Keep investing through them to get lower prices.

- Changing assets too often: Stick with your chosen investment. Jumping around defeats the purpose of DCA.

- Investing without research: DCA reduces timing risk, but you still need to choose quality investments.

- Not automating: Manual investing is harder to maintain. Set up auto-transfers and forget about it.

- Expecting quick results: DCA is a long-term game. You won’t see big gains in weeks or months. Think in years.

Final Thoughts

Dollar cost averaging is one of the best ways for beginners to start investing with confidence. It simplifies the process, removes emotional decision-making, and allows you to build wealth steadily. You don’t need a large amount of money, don’t need to be an expert. You just need a plan, consistency, and patience.

Whether you’re investing in stocks, crypto, or ETFs, this approach can help you grow your portfolio while minimizing the stress and risk that often come with investing. It turns volatility into an opportunity instead of something to fear.

Now that you know what dollar cost averaging is for beginners and how to use it, there’s no reason to wait. Pick an amount, choose an asset, and start your journey today. Your future self will thank you.

Disclaimer

This content is for informational purposes only and should not be considered financial advice. All investing involves risk. Past performance is not indicative of future results. Always consult with a licensed financial advisor before making investment decisions.